Retire a Millionaire now by following this plan.

Retire a Millionaire on Just $35 a Week

Not everyone has a big cushy salary. Plenty of folks out there work hard just to make minimum wage. Or maybe you make a decent salary but have suffered financial setbacks due to emergencies. Heck, even providing for a family of four can be expensive!

But that doesn't mean you can't save money for a comfortable future.

A Surprising Formula for Success

Typically, we talk about investing in percentages: Dave recommends contributing 15% of your household income into tax-advantaged retirement accounts to retire comfortably. Everyone’s 15% is different and may be big or small depending on your salary.

But what if we broke it down into a number that’s easy for everyone to relate to—a figure that could easily cover a dinner out or a week’s worth of daily super-sized lattes?

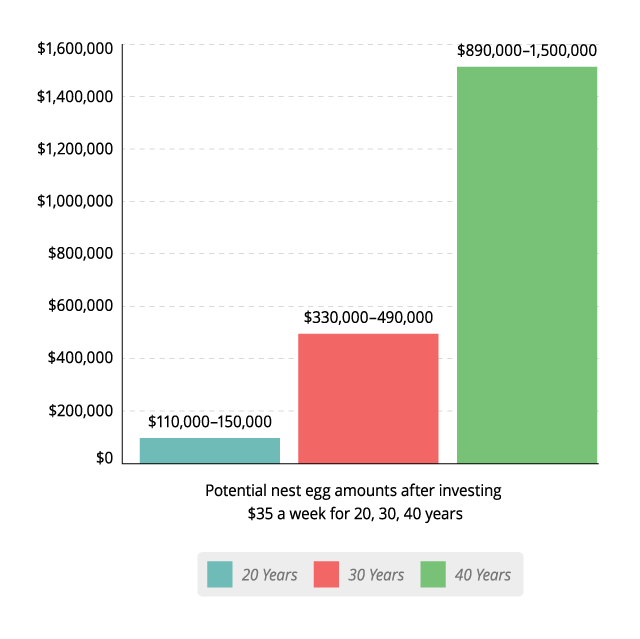

Let’s see what kind of future $35 a week could afford you if you invest in good growth stock mutual funds. That would be 15% of an approximately $12,000 salary—$3,000 less than what you’d bring home in a year if you worked 40 hours a week at the federal minimum wage.

- In 20 years, you could retire with $110,000 to $150,000.

- In 30 years, you could retire with $330,000 to $490,000.

- In 40 years, you could retire with $890,000 to $1.5 million!

Keep in mind that this example doesn’t take annual raises into account. You’re not stuck at today’s income. Work hard for your money and you’ll get raises along the way. Imagine how your nest egg could look if you increase your contributions as your income grows!

Related: Find an Investing Pro today!

Don’t Have 40 Years to Invest?

That’s okay! It just means you’ll need to roll up your sleeves and give it everything you’ve got in the time you do have. Here are some ideas to take your retirement savings to the next level.

- Pick up the pace. Add oomph to your retirement savings by bringing home a little extra bacon and rolling it into your nest egg. If you doubled down and contributed $70 a week, you could retire with $230,000 to $290,000 after 20 years and $660,000 to $980,000 after 30 years.

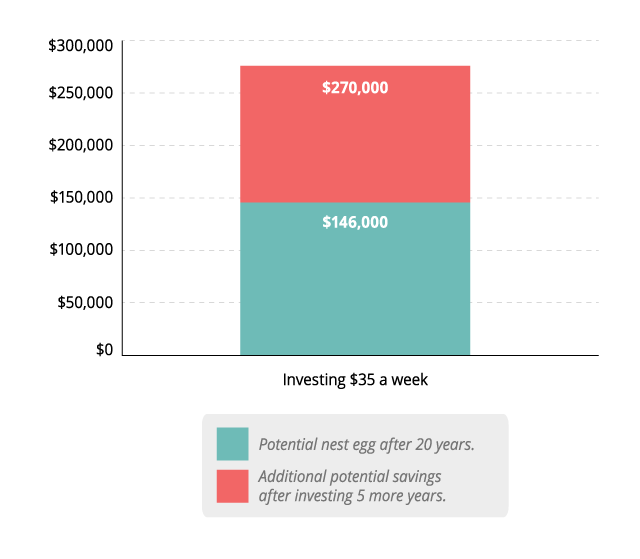

- Work a few extra years. There’s no rule that says you have to retire at 65. If you’re 45 years old, adding five more years to your timeline could boost your savings to $200,000 to $270,000 if you continue to contribute just $35 a week.

- Pay off your mortgage. This is a big one, but think about how much further your money could go without a mortgage hanging over your head. It might mean sacrificing a bigger home in the short term, but it will be worth it in the long term.

Make the Most of Your Nest Egg

Now that you know the difference $35 a week can make on your future, let’s talk about how to get the most bang for your investing buck.

- Clear your financial plate. You should be debt-free (except for your home) with a fully funded emergency fund before setting anything aside for retirement. It’s the only way to free up your biggest wealth-building tool—your income!

- Choose wisely. Put your money in good growth stock mutual funds with a long history of above-average returns. Dave recommends spreading your investment dollars evenly across four categories: growth, growth and income, aggressive growth and international.

- Stick with it. Your retirement fund is not a short-term investment. That’s the only money you’ll have when you leave the workforce. Consider it off-limits until you retire and don’t let a temporary downturn scare you into a decision that will lose you money in the long term.

Talk With an Investing Professional

You don’t have to bring in big bucks to win with money! And regardless of whether your income is large or small, talking to a professional helps. It doesn’t cost a thing to sit down with an investing pro and just look at your options. This person will take the time to explain their recommendations in terms you can understand so you can decide how to spend your hard-earned dollars.

Source: https://www.daveramsey.com/blog/retire-a-millionaire-on-35-a-week?

Comments

Post a Comment